In the preceding article, we articulated a high-level macro outlook for the energy industry at large. Focusing now on the global syngas industry the consistent theme will be the application of syngas technology in regionally specific deployments, but petrochemical production will be the driver for all conversion operations.

Directing attention to the world’s largest producer first, China looks to continue its domination of global syngas production as an answer to it energy needs, desire to curb emissions, and to supply its petrochemical demand. What many outside the syngas industry fail to realize, is that the Chinese are heavily reliant on coal-to-gas conversions for fuels and chemicals used as factors of production for terminal consumer and commercial products. With China’s coal consumption expected to peak around 2020, it should be expected that chemical consumption will continue to drive syngas development and consumption in the Southern Asia.

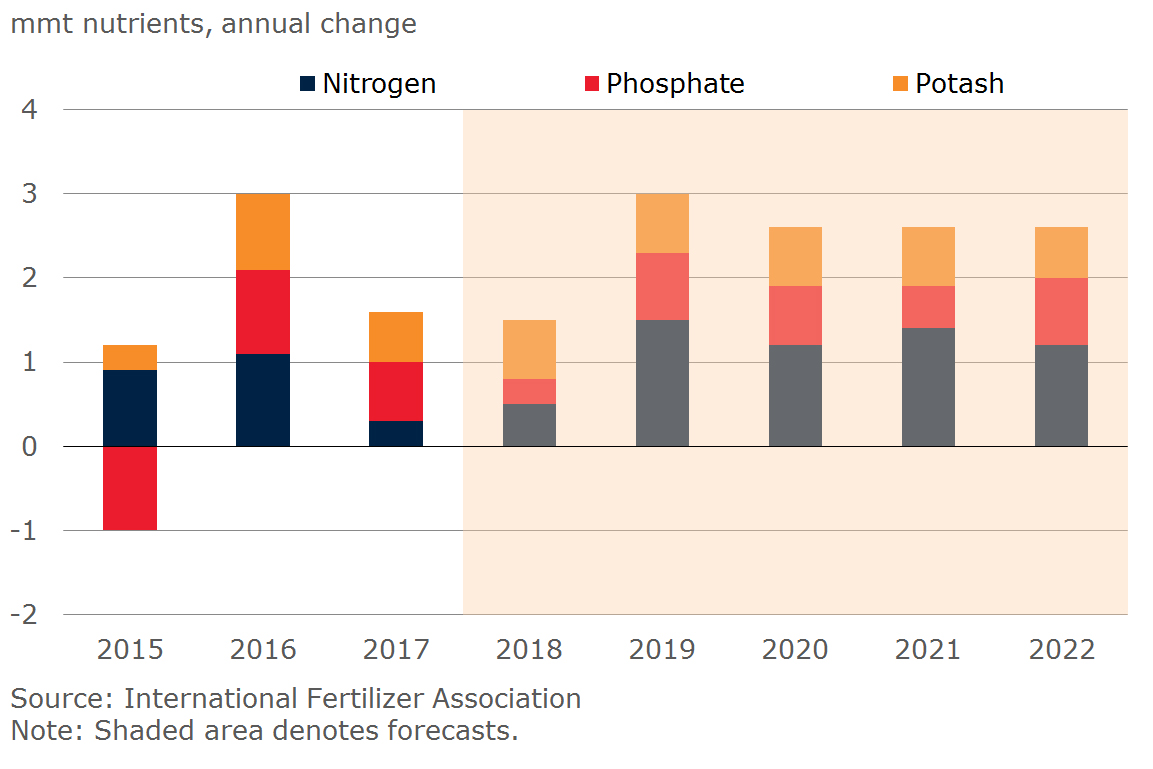

Looking to North America, the theme will be the capitalization of natural gas resources with few coal projects expected to begin. Coal is not as dead as what many have declared it, but it is at a point in its economic lifecycle that it could continue to slowly fade into the background of commodity demand or find new life as a factor of chemical production. In kind, Canada is looking to join the United States with increasing nitrogenous fertilizer production – the driver of the petroleum industry that will sustain oil and gas exploration past the hoped – for death of fossil fuel vehicles. Canada, especially, will continue to look to develop its heavy oil and coal resources due to the lower costs compared to U.S. crude and the need to blend with American crude to formulate a pipeline capable fuel.

In Europe, Brexit will determine a lot of how things will shake out. Not knowing if the exit from the EU will be under WTO rules or a one-off negotiated deal, the effects on syngas production and utility cannot be truly projected with so many unknowns at play. What we do know, is that in 2016 the United Kingdom was responsible for roughly 64% of Europe’s bio-mass fuel production. Finland is the continent’s next largest producer but losing access to 64% of total production will likely be difficult for the member nations considering they are so reliant on each other for energy production. With an energy supply being cutoff, even in the short term, look for Europe to replace the supply shortage with fuel from Russia or increased production from Finland where some firms have considered scaling up 388% to fill demand.

Moving forward, the world could be looking at the formation of a syngas renaissance. Depending on feedstocks, local infrastructure layout, costs and technology accessibility many nations across the world could breathe new life into old generation capacity with capture and high efficiency technology or see the rollout of new modular platforms for petrochemical production. The world needs cleaner, cheaper, safer technologies. Not just those that are deemed “green”. Syngas production utilizes the fuels at hand in cleaner applications and in many cases provide cheaper, cleaner, secure energy and consumer chemical production.

Website designed and managed by Cogo Interactive